Automotive AI—HMI Takes the Wheel, North America Sets the Pace

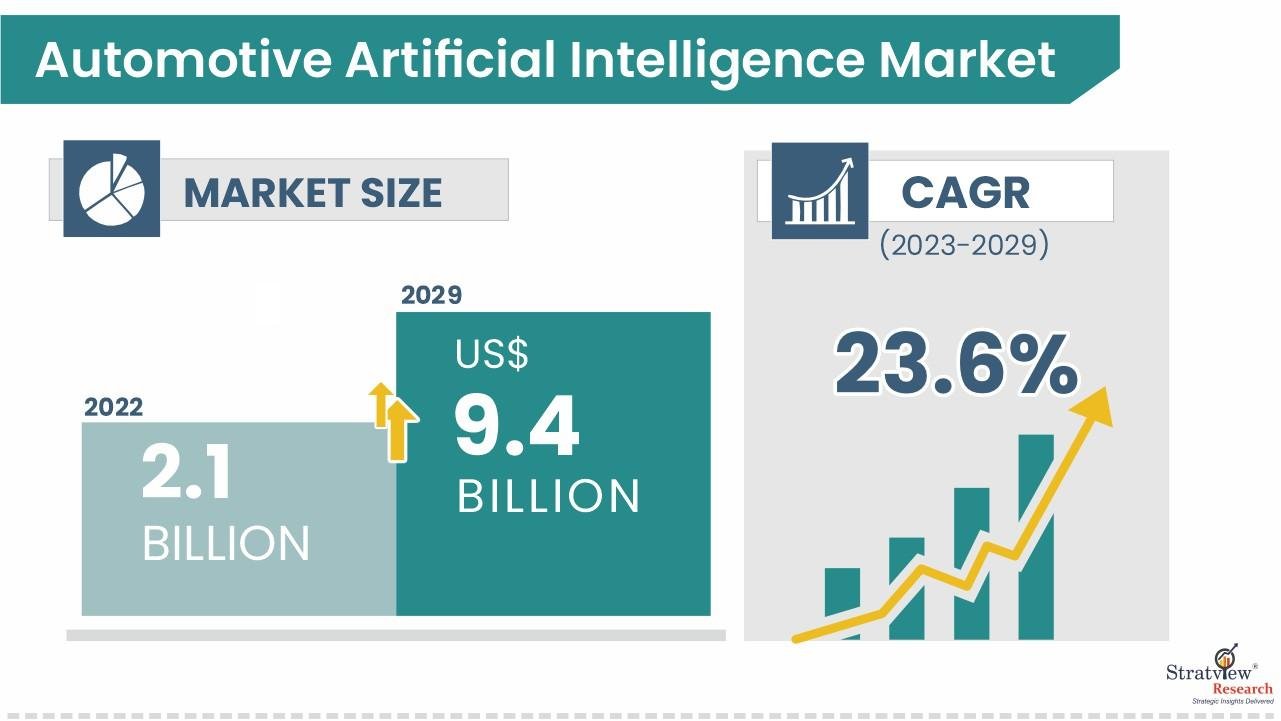

Automotive artificial intelligence (AI) has shifted from back-end R&D to front-line value creation, powering features drivers can see and feel—natural-language voice, driver monitoring, adaptive cruise, automated parking—and the complex perception/decision stacks behind higher-order ADAS and autonomy. Stratview Research estimates the automotive artificial intelligence market at USD 2.1 billion in 2022 and projects a 23.6% CAGR through 2029, reaching USD 9.4 billion.

Request the sample report here:

Drivers

A triad of forces is propelling adoption. First, user experience (UX) has become a competitive wedge. Carmakers are standardizing voice and gesture control, large displays, and seamless smartphone-grade interfaces. In Stratview’s application view, Human–Machine Interface (HMI) is the largest application segment—reflecting OEM focus on comfort, convenience, and differentiation at every trim level.

Second, machine learning (ML) is the workhorse technology. It underpins perception (camera/radar fusion), intent prediction, and personalization. Stratview identifies ML as the dominant technology segment across the forecast period, a signal that scalable data pipelines and inference optimization are now mainstream engineering priorities at OEMs and Tier-1s.

Third, electrification multiplies AI touchpoints. As EV volumes climb, AI helps extend range (eco-routing, regenerative strategies), optimizes battery thermal windows, and predicts component health—folding neatly into over-the-air (OTA) maintenance and lifecycle value. Stratview points to rising EV adoption as a specific catalyst for automotive AI demand, linking energy management and charging efficiency with the broader growth outlook.

Under the hood, the component stack is diversifying. Stratview segments components into microprocessors/SoCs, GPUs, FPGAs, memory & storage, image sensors, and biometric scanners, delivered as hardware and software offerings—mirroring the shift to domain and zonal architectures that centralize compute and enable software-defined features over time.

Regionally, North America leads during the forecast period, buoyed by a deep ecosystem of AV/ADAS developers, chip and cloud majors, and safety-driven regulation that accelerates feature standardization.

Challenges

Execution hurdles are real. Technical complexity rises fast with perception range, corner-case coverage, and redundancy targets; that stresses compute budgets, thermal envelopes, and cost of goods. Cybersecurity risk expands with connectivity—vehicles must protect model IP and data while preserving low-latency inference, which raises the bar on secure boot, partitioning, and zero-trust networking.

Regulatory and ethical issues remain fluid. Liability frameworks for higher levels of automation, disparate national rules on hands-off driving, and expectations around driver monitoring and data usage can create go-to-market asymmetries across regions. Stratview flags cybersecurity and regulatory/ethical considerations as key market challenges—issues that require both engineering and policy solutions.

Supply-side concentration is another watch-out. Advanced nodes for automotive-grade SoCs and GPUs are capacity-intensive; qualification cycles are long; and functional safety (ISO 26262), ASPICE, and automotive-grade memory endurance compound time-to-market. Finally, ROI discipline is essential: customers expect premium features at mass-market prices, pushing suppliers to squeeze TOPS per watt and per dollar without sacrificing safety cases or validation breadth.

Conclusion

The center of gravity in automotive AI is shifting from moon-shot autonomy to scalable features that delight customers today and lay rails for tomorrow. Stratview’s outlook—USD 2.1 billion (2022) to USD 9.4 billion (2029) at 23.6% CAGR—frames a robust trajectory led by HMI adoption, ML-driven perception, and EV-centric optimization, with North America setting the adoption tempo. Winners will pair efficient silicon and sensor stacks with production-grade software, rigorous safety/cybersecurity, and OTA roadmaps that compound value over the vehicle’s life. In short: design for everyday usefulness now, while architecting for autonomy later.